Feeling sanguine about stocks? Here is a data point that should give you pause. Via the AAII and James Mackintosh at the FT, holdings of cash are now at their lowest levels since March of 2000.

“If that date sounds familiar,” adds Mackintosh, “it should. The dot com bubble was just about to pop, and the S&P 500 hit levels not reached again for seven years.”

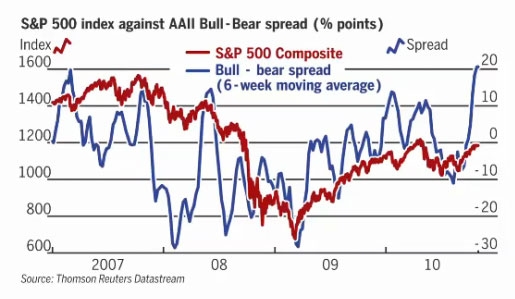

Mackintosh further highlights the “bull-bear spread” (blue line) as plotted against the S&P 500 (red line) in the multi-year chart above (click to enlarge).

The bull-bear spread is a basic contrary indicator that is most valuable at extremes. When bulls greatly outnumber bears — as represented by spikes in the spread — the market tends to run out of gas.

This makes sense because, when optimism peaks, those with an urge to buy have mostly done so. Conversely, the bull-bear spread did a great job of highlighting the March 2009 lows, which came at a pessimistic extreme.

As you can see, at current levels, the bull-bear spread is at record highs (with cash holdings at decade lows). Complacency is rampant. So why haven’t stocks roared even more? Because a good portion of that bullishness has been focused on corporate credit markets alongside equities.

Bulls argue that the S&P is still reasonably priced, based on a forward earnings multiple in the 12.5 range. But this assumption depends on a far more speculative one — that corporate earnings have not hit a cyclical peak. The twin threats of post-stimulus slowdown and housing double dip threaten this belief.

What really matters now is whether the U.S. economy is in true recovery or not. If the answer is “yes,” then the Fed is behind the curve and QE2 will serve as just another inflationary paper asset boost. If the answer is “no,” then the great body of evidence suggests QE2 will fail — and investors will be punished harshly for taking their complacency to such extremes.

Disclosure: As active traders, authors may have positions long or short in any securities mentioned. Full disclaimer can be found here.